Did your company recently change its directors, officers, stockholders, or office address? These changes are common. What is often overlooked, however, is that if they arise between annual meetings and affect information stated in the General Information Sheet (GIS), the corporation needs to submit an amended GIS to the Securities and Exchange Commission (SEC) within seven (7) days after the change occurred or became effective.

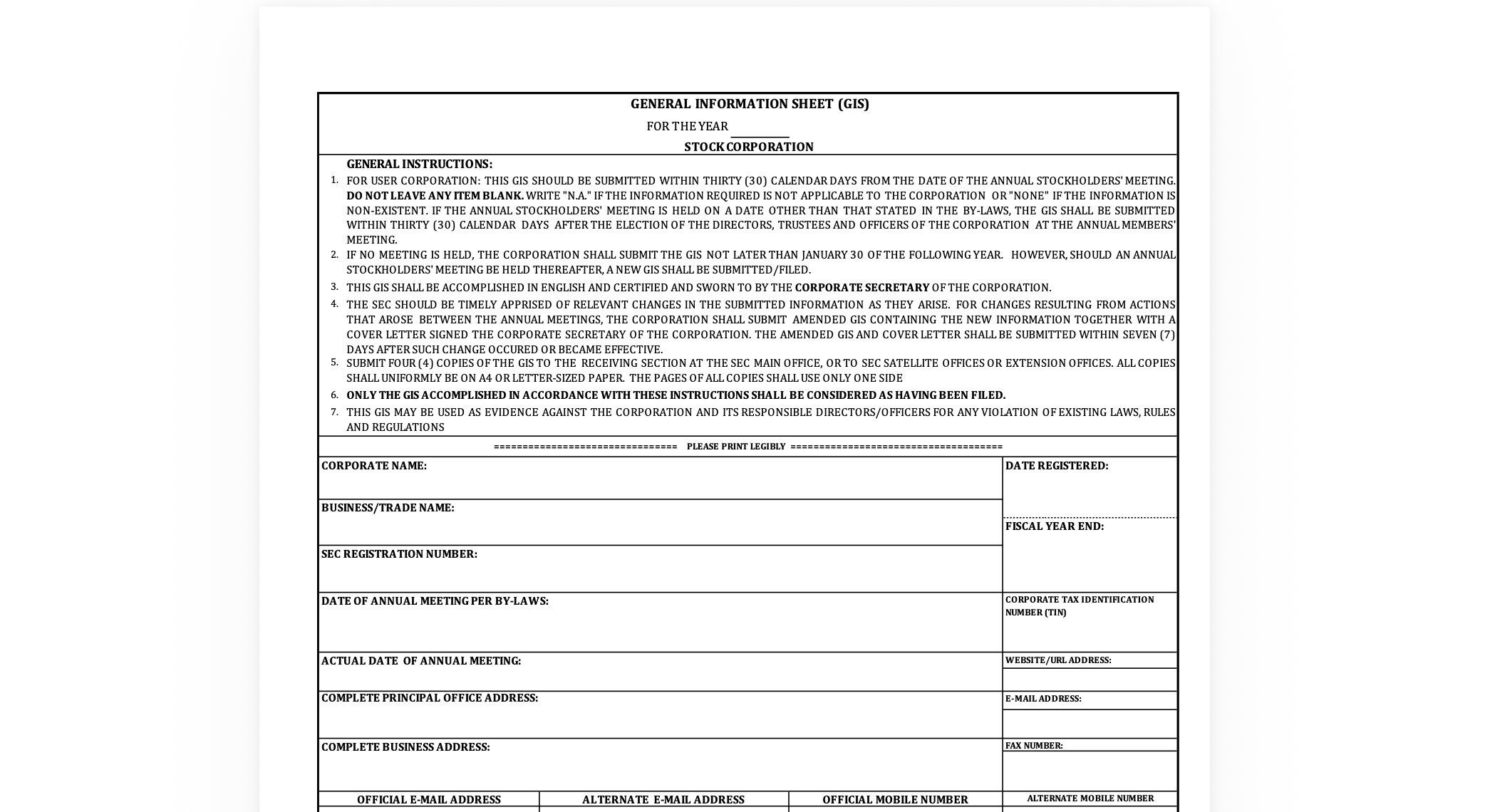

What is the GIS?

The GIS is one of the corporation’s key corporate records. It contains basic information about the corporation, including its corporate name, address, contact details, capital structure, names of directors, officers, and stockholders, investment of corporate funds, dividend declarations, regulatory licenses, and even the number of employees.

A common misconception is that the GIS is submitted only once a year after the annual meeting. In reality, if changes affecting the information stated in the GIS arise between annual meetings, an amended GIS is required.

Since the GIS is one of the corporation’s reportorial requirements with the SEC, outdated information in it can create compliance, governance, and transaction problems.

What changes commonly require an amended GIS?

Common changes include the following:

- changes in directors or trustees

This may arise from resignation, replacement, death, removal, expiration of term, or the election of a new set of directors or trustees. - changes in officers

This includes the appointment, replacement, resignation, or removal of officers such as the President, Treasurer, Corporate Secretary, or other officers reflected in the GIS. - changes in stockholders or shareholdings

These may result from transfers of shares, subscriptions, or other changes affecting the ownership structure reflected in the GIS. - changes in principal office or contact details

This includes changes in the principal office address, email address, or mobile number stated in the GIS. - other material corporate information reflected in the GIS

Depending on the circumstances, this may include changes in business purpose, par value of shares, or other corporate information that the GIS is meant to report.

What happens if the GIS is not amended?

1. Penalties and compliance exposure

Failure to timely file an amended GIS may expose the corporation to SEC penalties and other compliance consequences. More importantly, it can lead to broader regulatory issues for the corporation, including possible placement under delinquent status for failure to comply with reportorial requirements three (3) times, consecutively or intermittently, within a period of five (5) years, to suspension or revocation of the certificate of incorporation.

2. Due diligence issues

Corporations may encounter issues with banks, regulators, and other parties conducting due diligence, especially in connection with loans, licensing, and business transactions.

The GIS is one of the documents commonly used to verify the corporation’s disclosed information. If it is outdated, it can raise questions not only about the accuracy of the corporation’s records, but also about the corporation’s credibility.

3. Inconsistency in corporate records

An outdated GIS may also create confusion in corporate housekeeping. If the corporation’s internal records and SEC-facing records do not match, the inconsistency can eventually complicate compliance, verification, and future transactions.

Part of good corporate housekeeping, and more broadly good governance, is the proper maintenance of corporate records. An outdated or poorly maintained GIS may reflect negatively on the corporation’s compliance discipline and record-keeping practices.

Major caveat

One of the most common mistakes corporations make is to treat the updating of the GIS as sufficient to make a corporate act valid. This is wrong.

The GIS only reflects a change. It does not replace the proper step needed to make that change valid in the first place.

Any change reflected in the GIS must first be supported by the proper underlying corporate action. Depending on the matter, this may require proper documentation, board or stockholder approval, and in some cases, separate SEC approval or filing.

Below are typical scenarios before changes to the GIS may properly be made:

- Changes in corporate name, purpose, principal office address, authorized capital stock, or number of board seats require the proper board and stockholder approvals and an amendment of its Articles of Incorporation.

- A replacement of a director requires the election in a board or stockholders’ meeting, as the case may be, to fill the vacancy.

- A change in stockholders requires the proper documentation of the transfer, such as a deed of sale or assignment, together with compliance with any applicable tax requirements, such as securing an eCAR from the Bureau of Internal Revenue.

Final note

The GIS is not just a routine yearly filing. It is an important corporate record that should reflect the corporation’s current information. Changes in directors, officers, stockholders, address, or other material details may require the filing of an amended GIS, particularly when those changes arise between annual meetings.

At the same time, corporations should remember that the GIS does not by itself validate a corporate act. It only reflects information that must first be properly supported by the required corporate action and documentation.

If you need assistance in reviewing whether your corporation’s GIS needs updating, or in documenting the underlying corporate changes properly, you may refer to our guide, or schedule a consultation with us.